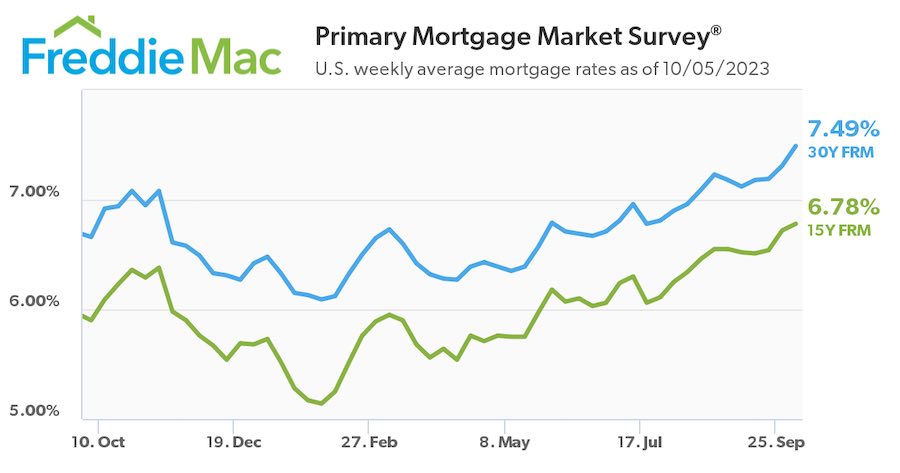

We have another record high for the last twenty years or so. Current rates are higher than they have been at any time in my 22-year career. Be very cautious. You might not be able to “date the rate” and “Marry the house” as some Realtors are suggesting.

For some owning a house is a short-term kind of thing. When a mortgage is involved short term home ownership is a win for lenders. The interest on mortgages is front-loaded making interest payments the highest in the first month.

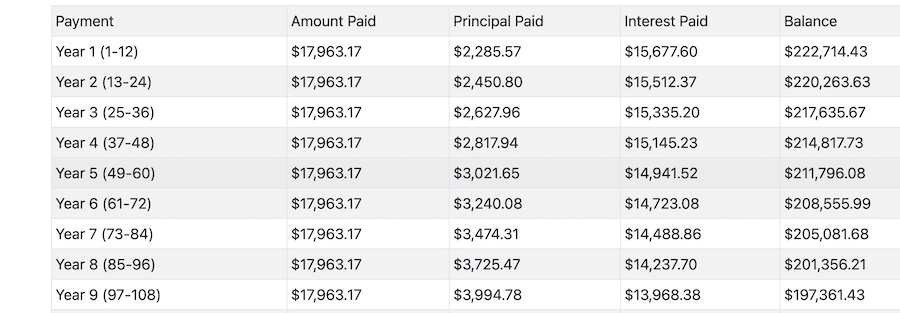

In fact, on a 7% 30-year mortgage with a 10% downpayment, it takes about 20 years before the monthly interest payment is lower than the monthly principal payment.

If the house is sold during the first five years of the mortgage the lender makes a lot of money. If someone else buys the house and gives a 30-year mortgage the lender makes even more money.

I support home ownership wholeheartedly but I often discourage home buyers who believe they will need to sell in a few years. Homeownership, or should I say mortgage ownership is more of a long-term kind of thing.

Amortization chart

Yes, interest rates matter. In the example above the borrower pays over 76,000 in interest during the first five years and $13,203 in principle. Sure home prices are rising and the buyer will have some equity after five years but they also had closing costs on the loan, a down payment and there will be closing costs and other expenses related to selling the house.

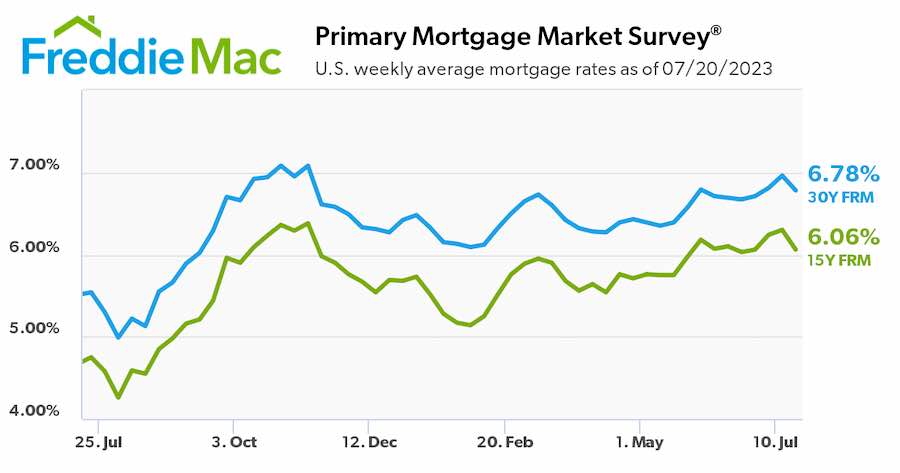

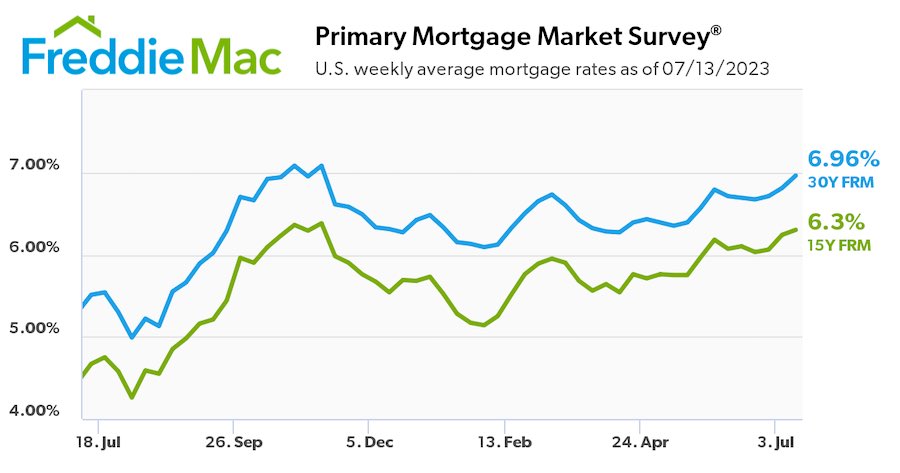

The 30-year fixed-rate mortgage averaged 7.09% as of Aug. 17, according to new data from Freddie Mac’s Primary Mortgage Market Survey. Last week, this mortgage averaged 6.96%, while one year ago it averaged 5.13%. The current level is the highest in more than 20 years.

Some have suggested that there may be yet another rate hike this year. I sure hope not. So far higher interest rates have not discouraged home buyers as much as home sellers who are staying put.

I know I wrote about how rates were headed in the right direction. They did go down a little but after last week’s rate hike by the federal reserve, they went up to 6.81% for the 30-year conventional mortgage. (Freddie Mac)

That is high, especially considering how expensive houses are. Last week I was talking with some older homeowners who pointed out that when they bought a house rates were over 8%. At the time one of them had a job that paid $3.50 an hour and the house cost $15,000. The house cost about the same as two years’ income.

The table below shows how much income is needed to buy a house in Minnesota. The numbers are provided by Minnesota Housing Agency.

Mortgage interest rates are in the news a lot these days. Interest rates matter. Housing was already expensive before the rates went up. Mortgage interest rates have gone down a bit which is better than up but they are still high.

The rates are not slowing down home sales but they are causing homeowners who are paying less interest to stay put which means they are not putting their houses on the market.

Personally, I would hold off on buying a house until the rates go down but I am in the minority.

Mortgage Interest Rates

What was I thinking? The Federal Reserve raised rates and as of July 27, 2023, the 6.78 on the chart is 6.81 – that is high. Experts claim this is the last rate hike. We shall see . . .

I mostly only write about mortgage interest rates when they are high or low. Last week they went up. I would call them high at close to 7%. The rates don’t seem to be slowing home sales down. probably because there are more buyers than there are houses on the market. Home prices remain high and are still rising.