There just isn’t anyway to sugar coat this. Mortgage interest rates are high. They will go down and when they do you may not be able to refinance and get a lower rate on your loan and if you do refinance the interest portion of your payment starts all over again. Borrowers pay the most interest on the first payment.

That means more interest and less equity. Anyone who reads this blog knows that I am in favor of homeownership. I am not in favor of debt or paying interest. Less debt means more freedom and more choices. Rates will come down again.

In the U.S. Mortgage debt is increasing and so is credit care debt. We owe, we owe, it’s off to work we go . . . .

Those low mortgage rates and the recent mortgage interest rate increases have caused people with low interest rate mortgages to stay put. Who wants to trade in their 2 to 4% rate for 7% or 8%?

Higher interest rates are also making housing more expensive which is contributing to inflation which is why interest rates are being raised.

Rates are likely to go down this year. This is an educated guess but once rates are around 6% people will be more interested in moving again which will increase demand and drive up home prices.

Higher home prices will contribute to measures of inflation which will prompt the Federal Reserve to increase interest rates.

Mortgage interest rates are too high and so are home prices, which rose due to high demand and low rates. Some real estate professionals are advising their clients to buy a house even though rates are 7%ish.

“Marry the house, and date the rate”. This catchy phrase has become popular advice and a catchy phrase since the Spring of 2022 when mortgage rates increased to 20-year highs.

The phrase “Marry the house, and date the rate” means you’re committing to a long-term relationship with the house you love. But you can dump the interest rate when you refinance.

Not so fast. Rates will remain high for a few years and it will take a few years just to build some equity at today’s prices. In fact, you can’t really date a rate. Well maybe you can but you don’t get to just decide when to date another rate.

When a borrower refinances to a new rate they start all over making mostly interest payments. People who have been laid off generally can not refinance. There are fees and closing costs too. In most cases, a borrower would need to own the house for at least three years and rates would have to go down by 2%. Good luck with that.

When my husband and I bought our first house rates were over 8.5%. At the same time houses were less expensive back then and our monthly payments were just a little more than rent.

We can not assume that home values will always rise and that rates will go down soon. Housing prices can go down or stay flat and rates can go up. In fact, sometimes renting makes more sense than buying. A home buyer could date an apartment and eventually marry the right house at the right price.

Typically the real estate agents promoting this phrase “Marry the house, and date the rate” either don’t know any better or are a bit sketchy.

There are funds available for downpayment assistance for home buyers. Especially first-time homebuyers and first-generation home buyers. By the way, often people who have not purchased a home in the last three years qualify as first-time home buyers.

There are programs for specific areas like the whole city of St. Paul or Minneapolis. My husband and I bought our first home using a program through the City of St. Paul. Through the program, we got a forgivable downpayment grant and a lower interest rate. I can still remember how thrilled we were to be homeowners.

Ask your lender about down payment assistance programs and other programs you might be eligible for. Some of these programs will run out of money long before the year is over so hurry.

I have helped several home buyers successfully use downpayment assistance. I believe in these programs because they made a huge difference in my own life.

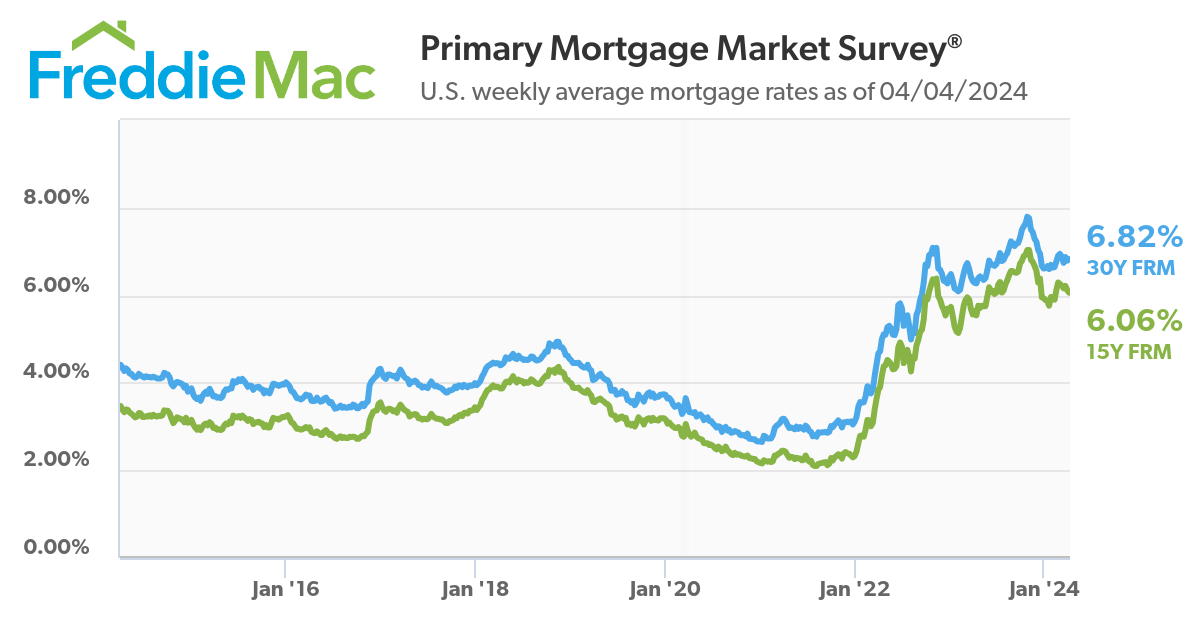

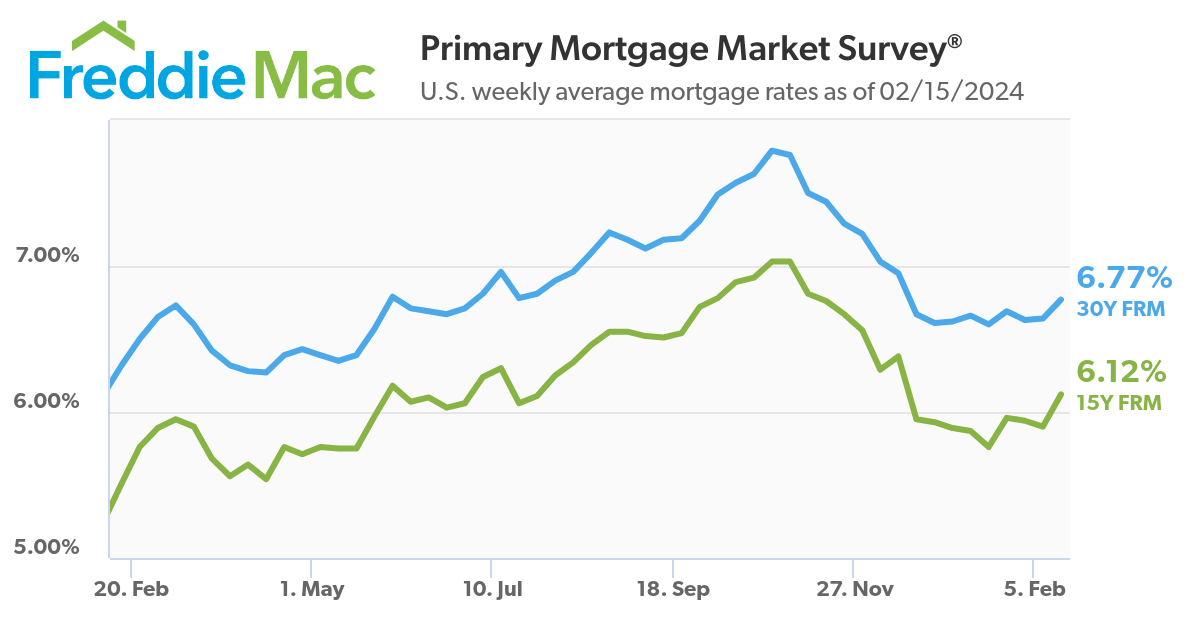

Mortgage interest rates go up and down slightly all the time. These days rates are high so as soon as they go down a little that is newsworthy. Personally, I don’t see any room for optimism when it comes to mortgage interest rates that are higher than 5.5%.

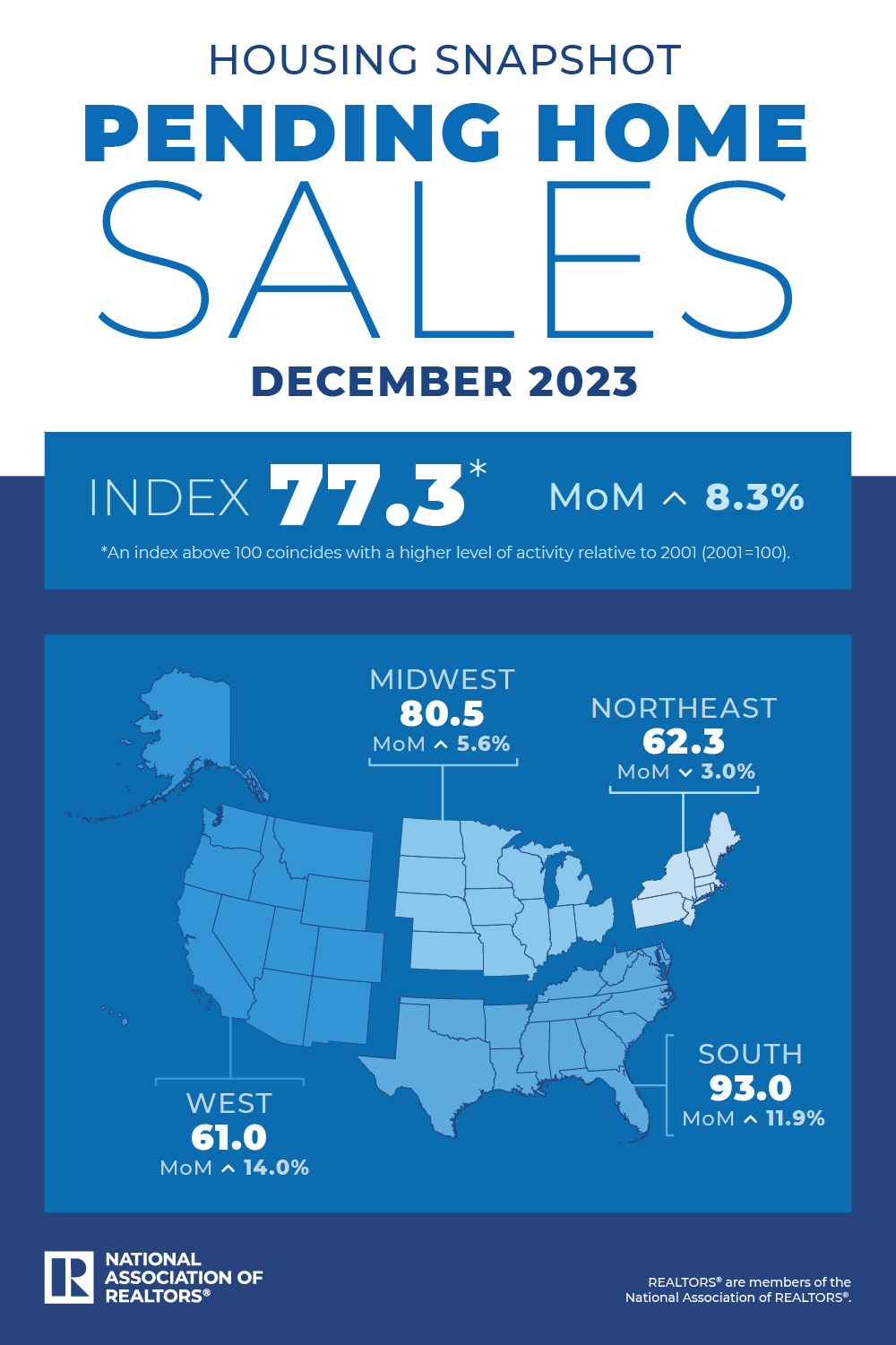

Apparently home sales were up in December from November. There is already talk about having hit some kind of a “bottom” when it comes to the number of home sales. I’ll go out on a limb and say that the sale of existing homes may be slightly higher in 2024 than in 2023 but I expect home sales to go up as interest rates go down. Keep your eye on those rates. According to Freddie Mac rates were on average above 6.5% last week on a thirty-year conventional mortgage. When they get to 5.5% and below we will start to see more activity in the housing market.

Here is the reason why: “The Mortgage Bankers Association reported the national median payment applied for by purchase applicants decreased last month to $2,055 from $2,137 in November.”