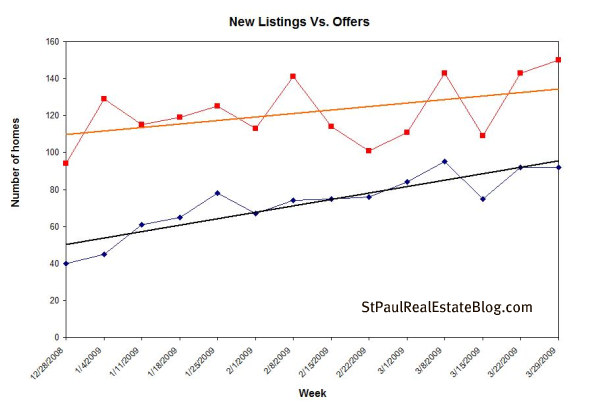

The red line on the chart above shows the number of homes that were listed for sale through the Regional Multiple Listing Service (MLS) each week since the beginning of the year. The blue line shows how many homes had offers made on them that were excepted by the sellers during the same week. Some of the homes have closed and some have not. Pending sales and listings are a metric used to measure the health of the real estate market. Real estate is local and these numbers are for St. Paul Minnesota. If you own real estate in St. Paul, or if you plan to buy this data is more useful than national numbers or numbers.

The chart looks better each month. In 2007 the two lines were going in opposite directions and the inventory of homes on the market grew, while at the same time the number of home sales fell. By mid 2008 the inventory of homes on the market started to go down, but buyer activity remained flat.

On this chart the trend lines are going in the same direction. Listings are up and so is buying activity, partly because it is spring but the trend line for buying is going up a bit sharper than the listing trend line. The inventory is being absorbed. More than 50% of the sales have been foreclosures and average prices are down. I will show those numbers on Thursday.

A combination of low prices, the $8000 dollars tax incentive and very low interest rates has gotten some of the buyers off the fence. The banks are still difficult to work with. They have lowered prices but they also SCREAM AT US IN THE AGENT REMARKS on the MLS in all capital letters advising us that our clients will have to pay to have the home "de- winterized", and some are charging buyers a fee for submitting an offer. I don't think the banks are charging the fee I suspect it is the agents. They are also requiring buyers to be responsible for repairs mandated by the city. Banks can't sell real estate but at this point 60% of the homes on the market are in some stage of foreclosure, and they are indeed selling.

The banks lower the prices and sit on offers until they get one they like. My advice to anyone buying a bank owned home is to have patience. There are some great buys out there as long as the buyer is willing to put up with a bunch of bureaucratic bull shit B.S. I can't think of any other situation where a person would be spending ten's of thousands of dollars and be treated like like . . . never mind.

Have prices hit bottom? Hard to say. The numbers are a bit distorted at this point because even though activity has picked up in all price ranges the lowest priced properties that usually need repairs are the homes that are selling the fastest.

Hehe-

The banks have many more painful lessons to learn.

We must consider several key points:

The Federal Government is throwing all their muscle into lowering mortgage rates. This is effectively a subsidy. The minute the government backs off, rates will rise, crushing house prices.

Possibly the government will make rate manipulation permanent. This will come at an economic cost as government finances are tied up covering mortgage debt.

What will happen to prices when the tax credit ends? Will they extend it? Perhaps. Remember what happened after 911 when the carmakers did 0% financing? People expected it forever. The same will be true of other incentives. When they end, buyers will lose interest until the ‘happy hour’ pricing returns.

It is no different than the bank bailouts. One is never enough. As each fresh group of buyers is used up, greater incentives are needed to lure in the next group. Lawrence Yun’s nose will be as long as a broomstick before prices recover.

Jobs. We are headed for record unemployment. Replacement jobs, when they arrive will not pay at the old rate. House prices will always be a function of wages, even in a zero-down environment.

The house price question will only be answered after the jobs and wages question has been answered, and not before.

Those who are watching house prices are wasting their time while unemployment numbers are still up for grabs.