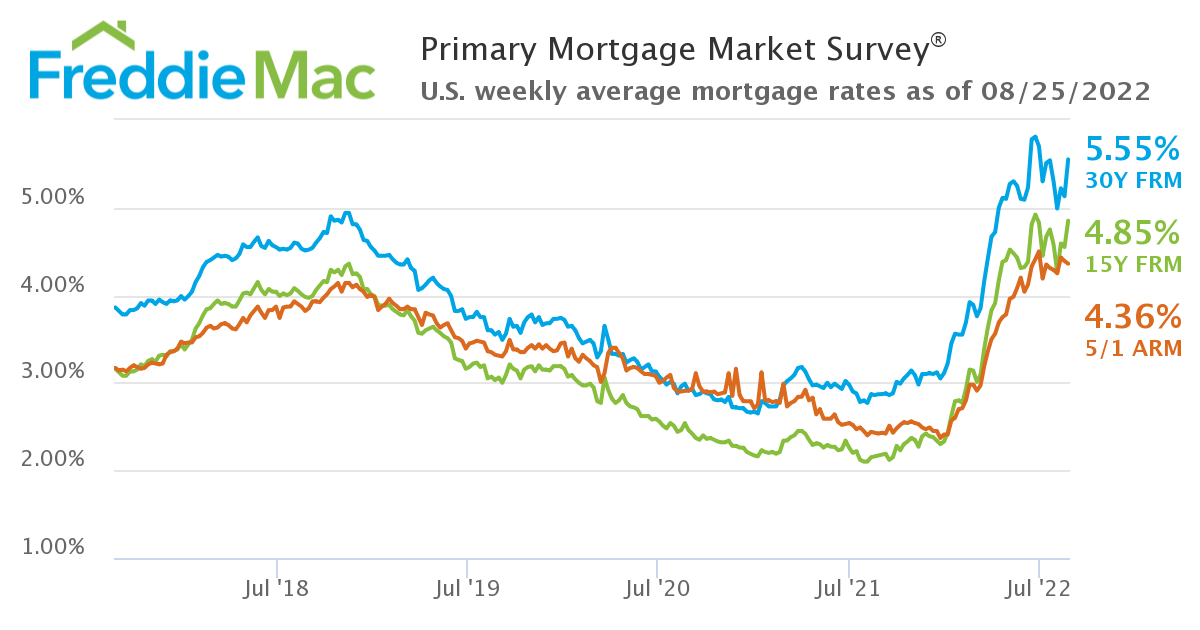

Don’t expect interest rates to go down. By historic standards they are low. Federal Reserve chair Jerome Powell told us on Friday that the Federal Reserve will fight inflation and there will be some pain. Mortgage rates went up last week but are slightly lower than they were in June. Housing prices are still rising the rates may slow that down a bit.

It won’t be the wealthy who feel that pain it will be the poor. Powell didn’t say that but we all know that it is true.

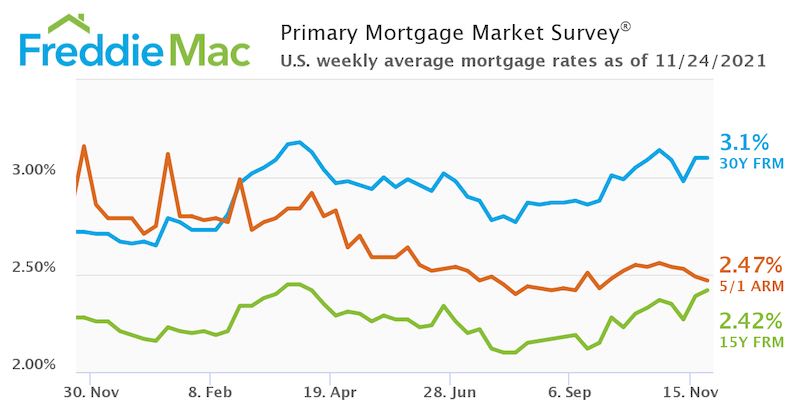

Current mortgage interest rates

As for the rates in the chart they are averages and they are the rates that borrowers with good credit ratings get.

Weakening demand for both purchase loans and refinancing last week brought mortgage applications down to the lowest level in 22 years, according to a weekly survey by the Mortgage Bankers Association.

Rates may go up again this year which should mean that home prices will level off a bit. I say should because in this wacky world we live in things don’t always work the way they used to.

Back in 2006 before the great recession which was brought on by the housing market crash, rates were around 6.5% for most of the year.

There really isn’t any way to soften the blow. Housing is more expensive when mortgage interest rates go up.

Rates actually went down slightly. They are lowish if we consider rates over the last 40 years but with housing prices at an all-time high, housing is less affordable. People who have mortgages at lower rates are likely to stay put rather than move. The refinance business is pretty slow these days.

Mortgage rates went up to levels that we haven’t seen since 2009. It should be noted that 2009 was during a recession and housing market crash. Housing prices have more than doubled since then here in the Twin Cities and in other parts of the country. In the early 2000’s rates were at 6 and 7% but houses did not cost as much as they do today.

It is likely that the higher rates will cause homeowners to reconsider selling. It is too soon to tell if it will dampen buyer enthusiasm. Homebuyers are making offers and competing with one another to make the highest offer so that they can buy a house. . . at least as of this week.

Some folks are able to buy a house without giving a mortgage. In the last few years, cash offers have become more common.

Even with a cash offer buyers need to have some kind of proof of funds, maybe a letter from a financial institution.

For example, cash to buy a house may come from a combination of cash from a savings account and a retirement fund. The buyer could get a letter from the bank and from the investment fund stating that they have funds. Another option is to use bank statements but I always encourage buyers to redact the account numbers.

Letters work because they usually include an email address and a phone number which makes them easier to verify with the financial institution.

Cash buyers sometimes assume that all they have to do is say they have the money and the sellers will just trust them. Over the years I can think of several times that people told me they had money that they didn’t actually have. They may be expecting an inheritance or a settlement from a lawsuit or some of the cash is coming from a gift from a relative.

If you plan to purchase a home using cash get something in writing that can be used as proof of funds and be prepared to submit it with your offer. Savvy sellers won’t just take your word for it.

It takes a long time for most of us to actually own a house. At first, the bank or mortgage lender is the primary owner and we make payments. Eventually, homeownership is possible.

Mortgage interest rates have an impact on the housing market. When rates go up some buyers will get cold feet even though the rates are only slightly over 3% on a thirty-year conforming mortgage. The common wisdom is that rates are more likely to go up than down because inflation is on the rise.

Rates were higher in March of 2021 at an average of 3.17% for a 30-year mortgage. In March of 2020, they were around 3.65%.

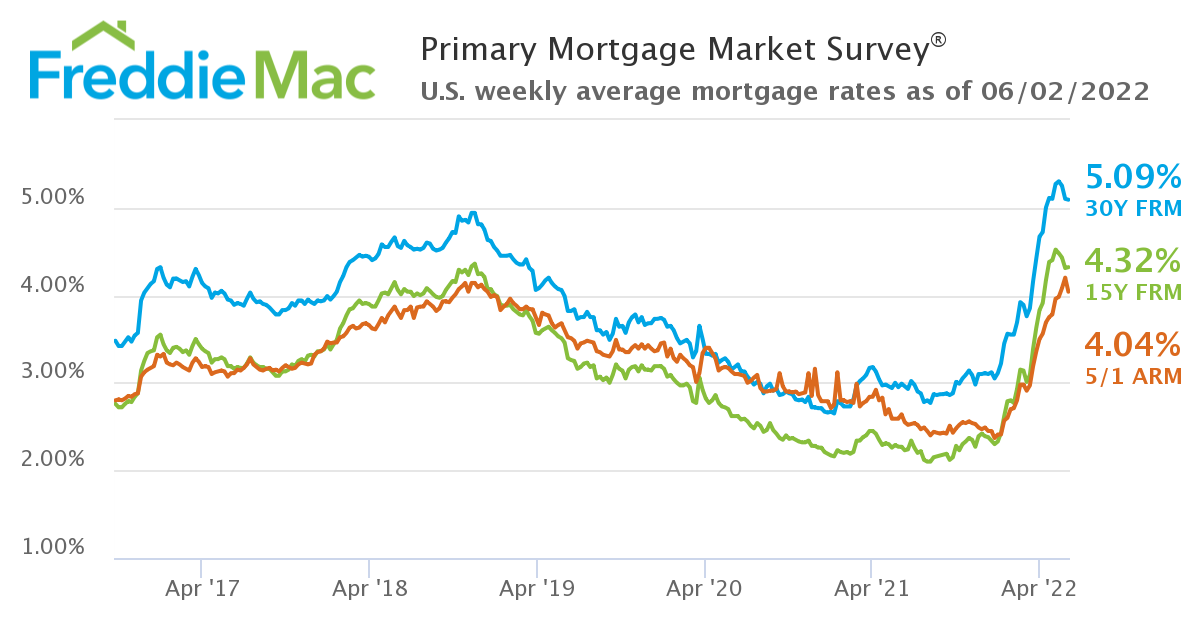

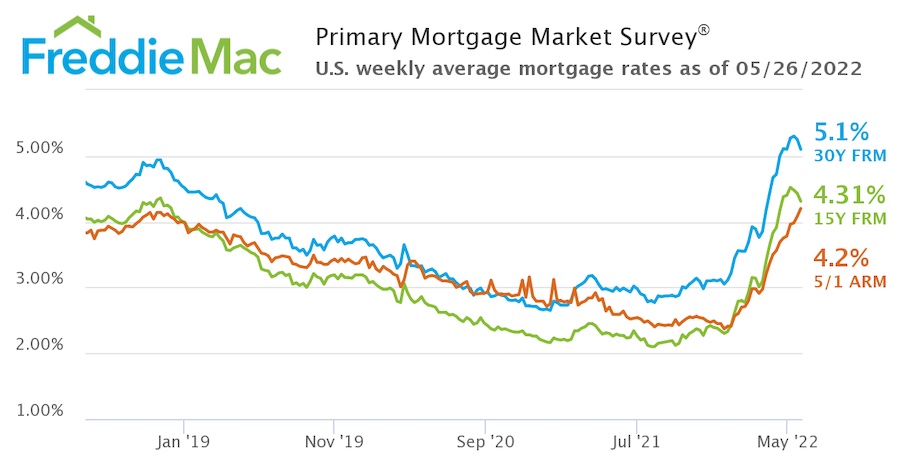

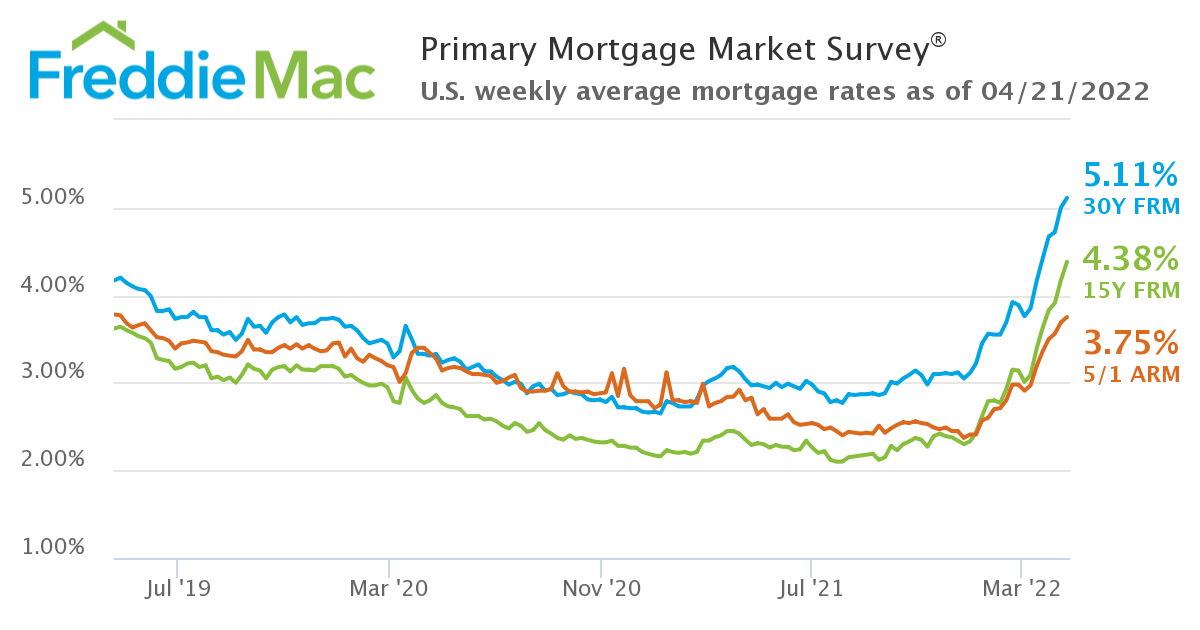

Primary mortgage rate survey

This could be a better time to buy a house than next March when rates will be higher.