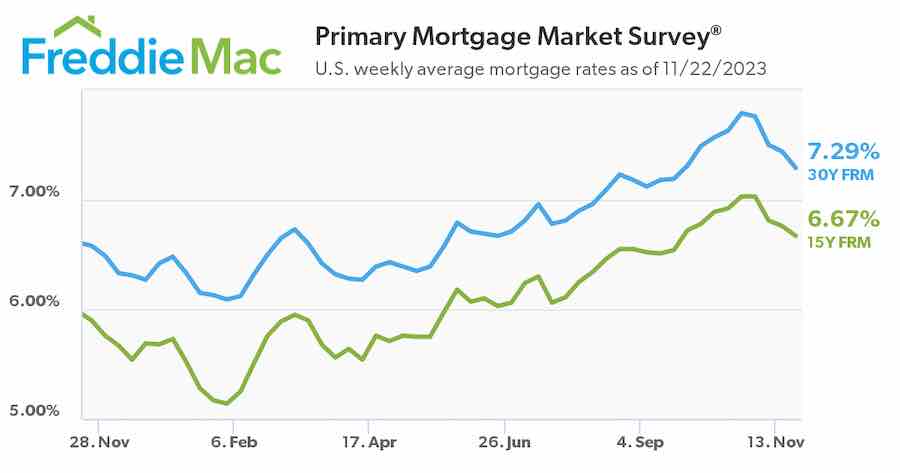

Yes, mortgage interest rates are still ridiculously high but they are going in the right direction. Just because your parents had to pay 8%, or 9% or more doesn’t mean 7.29% is a deal. Houses are proportionally more expensive today than they were in the 1980s. Houses have gone up by 310% since 1980. Wages have gone up about 17.5% since 1980.

If a lender or a real estate agent suggests that home buyers are dating the mortgage but marrying the house just walk away. It costs money to refinance and if housing prices level out or go down home buyers wishing to refinance may find themselves with no equity, or worse.

Mortgage interest rates

Cash buyers can take advantage of softer prices during the holidays and fewer buyers to compete with.

Most parents want only the best for their children. When my firstborn came along we were in a one-bedroom apartment and her first bed was a dresser drawer. She had everything she needed and got through it unscathed. We were able to move to a two-bedroom apartment shortly after her first birthday which was nice for us. Our son was born the following year and we stayed in that two-bedroom apartment until he turned 5.

Babies do not need a lot of space. Parents on the other hand may need the space. Children need many things and sometimes buying a house is so expensive that there isn’t enough money left for anything else so we compromise. I think my children did just fine even though they lived in a small apartment and had mostly second-hand clothes and toys during their first five or six years.

Children can survive and even thrive while living in a small house.

“The U.S. housing market is missing about 320,000 home listings valued up to $256,000, the affordable price range for middle-income buyers (households earning up to $75,000).

Middle-income buyers can afford to buy less than a quarter (23%) of listings in the current market. Five years ago, this income group could afford to buy half of all available homes.

Among the 100 largest metro areas, El Paso, Texas; Boise, Idaho; and Spokane, Wash. have the fewest affordable homes available for middle-income buyers. Conversely, three Ohio metro areas – Youngstown, Akron, and Toledo – have the most.”

I find walkability scores on many real estate websites. They can be kind of misleading or maybe they do not prioritize errands that we make frequently. For example, I found a house with a high walk score even though the closest grocery store is more than 4 miles away.

Using google maps and google street view is also a great way to determine walkability. It is easy to find nearby shops and to see if there are sidewalks or if there are busy intersections that are hard to cross on foot.

It doesn’t matter all that much if the businesses that are close by are businesses that you don’t use or need to walk to. For instance how often does a person walk to an insurance company or a tire shop?

Having ice cream within walking distance is a plus. In my neighborhood, there isn’t any ice cream but no one lives more than a block or two from a bar, brewery, or taproom. I have been told that beer is sustainable but ice cream is not.

The suburbs are not about walkability they were designed around the automobile and all errands require a car.

Anyone who says that interest rates don’t matter isn’t being truthful. Sure a person can buy a house at today’s rates ad then refinance when rates go down but that means paying less on the principal for longer.

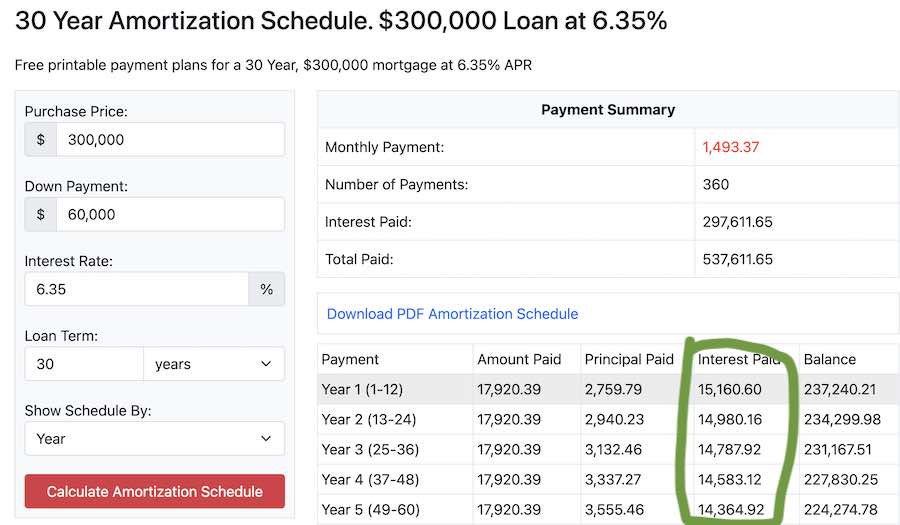

Mortgage interest is front-loaded. When the borrower refinances they start all over and make payments that are mostly interest. Ask Google to amortize a home loan for you and run some scenarios. Mortgages are seriously expensive. In the example below sometime in year 20 of the 30-year loan the principal payment is more than the interest payment. By the time the loan is paid off the borrower has paid $672,014.56.

Is a house a good investment? Not always. Owning a house free and clear has some advantages but often when it is sold the proceeds are needed to pay for housing. Please borrow responsibly.

It is possible to refinance over and over and pay mostly interest on a mortgage and very little on the principle. The monthly payments may end up being lower but who wants to pay a mortgage for 25 years and still owe most of the principle?

If you are a home buyer and you are getting information from the NorthstarMLS, there is a disclaimer on the information: “Information Deemed Reliable But Not Guaranteed”.

If you are searching homes for sale on almost any website the data is coming from the Northstar MLS.

Some of the information is more reliable than the rest. Generally, the address, including the city and state the property is located is accurate. The listed price is likely to be accurate too. It is very hard to list a home in the wrong school district or in the wrong county.

Taxes and assessments are easy to verify by checking county and city websites.

Room sizes and measurements are notoriously inaccurate but I don’t find many that are so far off as to raise alarm. The foundation size and total finished square footage are sometimes wrong.

Association dues for condos are not always accurate but the association will provide an accurate amount in writing.

The number of bedrooms isn’t always accurate but Realtors are expected to provide an accurate bedroom count. I have seen houses listed as two-story houses that are really 1.5-story houses. It is usually pretty easy to tell from the picture.

At some point in the late 1880s, there was a fire and some tax records were destroyed. For the most part, we don’t know how old the houses that were built before 1885 are. The oldest houses will have a construction date of 1885.

Tax records are not always accurate either. Appraisals are a much better and more accurate source of information about square footage and room sizes. The lot sizes in the tax records seem to be fairly accurate.

People sometimes make mistakes. Listing information can go from the owner to an agent to clerical staff who actually enter it into the MLS.

I once had a client cancel a purchase because the house was 300 square feet smaller than what was listed in the MLS. The house was still big enough but the buyer was angry that he had been deceived.

The information in the MLS is deemed reliable because we are expected to put accurate information in the system. There is a link on each listing that real estate agents see and can click to report incorrect information so that it can be corrected.